Operating a successful small business requires an innovative approach to your business, openness to change, and the ability to implement those changes. When a small business is in the “growth” stage, wearing the many hats can become difficult for the business owner leading the business. Most small business owners feel they need to be in every aspect of their business to ensure its continued success, however this thought process is not always the best course of action.

Take accounting and bookkeeping for example. Many small business owners spend the majority of their time working in their businesses, that when it comes time to work on it (the accounting, bookkeeping stuff) they are exhausted from the work, source documents have been misplaced and other important information has been forgotten. Some business owners then chose the option of hiring a staff person to do the “grunt” work. Accounting is the foundation of any business. There is virtually no action you can do in your business without it creating an accounting transaction. From source document to financial statements and analysis, a small business owner needs the support of a capable, consistent, compliant partner. An outsourced accounting partner is the bridge to your small business success. Outsourcing your accounting provides you with the confidence that your financial records will be handled correctly from start to finish. You also will have a higher level of expertise for situations that require more than just “grunt” work, and your information can be processed faster with cloud technologies allowing you real-time access to your data. If you are a small business owner still struggling to keep up with the accounting and bookkeeping tasks in your business, then maybe it’s time to build a bridge to your success with outsourced accounting.

0 Comments

While getting in my morning run at the local high school track, I came across a notice informing parents that summer football camp would be starting next week with practices starting at 7am -1pm (have to start early with the hot summer days in the south). This got me thinking about how many high school football teams prepare for the upcoming season with summer practices, cardio and strength training and of course class work (except in this case it’s watching film and learning the playbook). As you can see, many high school football teams are not taking off this summer.

Another team that is not taking off for the summer is the IRS, and it seems that their playbook gets more complicated year after year. As a small business owner, you need to also “train” in the off-season so that your small business will be ready. Just like the football team, preparation before the season is a key component to success. You need to come up with tax strategies in your playbook to save your hard earned money. The summer is not the time to take off so use the “down” time and the calendar to your advantage. The summer football camp also got me thinking about a tax strategy that can help small business owners pay for the football camp via income shifting to their kids (add this one to your tax strategy playbook). Hiring your kids in your small business will shift income to a lower tax bracket and at the same time allowing the football camp payment to be a business expense. For more details on hiring kids in your small business be sure to read the chapter, How Employing Family Can Cut Taxes in my book “Expensive Tax Mistakes That Cost Small Business Owners Thousands” on Amazon. So use the summer to your advantage as a small business owner and hire your kids. Just be sure that their work schedule does not conflict with football camp.  With the Memorial Day holiday in the rearview mirror, many small business owners and entrepreneurs and busy planning their holiday vacations and many other summer activities. Another planning activity that really needs to be on every small business and entrepreneur’s list is tax planning. If you are like most small business owners and entrepreneurs, you waste thousands of dollars every year in taxes you don’t need to pay. You then grumble about it on April 15 . . . then wait until next year to get smacked again…you see a pattern here. The sad truth is, it doesn’t matter how good your tax accountant (let’s call him “Fully Depreciated Frank”) is with a stack of receipts on April 15. The key to beating the IRS is tax planning. The summer is a great time for tax planning. As a small business owner and entrepreneur, has “Fully Depreciated Frank” contacted you with answers to all of these questions?

If not, you need to go to Amazon and get our new book “Expensive Tax Mistakes That Cost Small Business Owners Thousands”. The book reveals the mistakes and missed opportunities that can cost you thousands in tax; then shows you how proactive tax planning can rescue those wasted dollars. Stop by Amazon now and stop making those expensive tax mistakes that make you hotter than the summer heat.

We all know a happy employee can increase your bottom line. Today on the local #FOX5ATL morning show there was a segment about the new Fortune 100 list of best places to work and the reasons these companies made the list (citing a happy work environment, fair pay, perks, benefits). Of course we are talking about large corporations, because as small business owners and entrepreneurs, OUR business is the best place to work so give yourself a pat on the back small business owners and entrepreneurs you made the list!

The morning show probed deeper on their social media network's "Question of the Day" asking what kinds of perks would people like. The answers were typical and pretty much validated the Fortune study. Mind you I am listening to this in the background as I manage the workflow of the early season tax returns in our virtual office....wait is that a perk? The question did get me thinking of ways small business owners can make their businesses the best place to work for them and their employees. one of the major ways is to offer benefits and perks to you and your employees, however many small business owners and entrepreneurs do not offer benefits because they think they are to expensive and/or difficult to implement. Did you know that by not offering perks and benefits your are more likely than not losing money instead of saving it? By offering perks and benefits you and your employees will have the opportunity to write off many of the expenses that you currently can't (or have been capped by the IRS). Making the most out of your tax deductions, credits and income shifting are just a few of the tax strategies outlined in my recent book Expensive Tax Mistakes That Cost Small Business Owners Thousands that can be found on Amazon. Be sure to pick it up and find ways to offer perks and benefits that will keep you and your employees on the list of best places to work.  2013 has been a big year for taxes. Earlier in the year, Congress passed legislation averting the so-called "fiscal cliff," and many of the "Obamacare" changes have taken effect, or are about to. While few of us who watched the process would consider it Washington's finest hour, we now have answers to many of the questions that have made proactive planning so difficult over the past few years. And now, with just 20 days left in 2013, it's time to review the "deals" the IRS is offering and start to plan.

Here are the highlights: • First, the Bush tax cuts are permanently extended for income up to $400,000 ($450,000 for joint filers). Ordinary income above those thresholds is taxed at 39.6%, while qualified corporate dividends and long-term capital gains above those thresholds are taxed at 20%. • Next, the 2% payroll tax "holiday" of 2011-2012 is over. This can mean over $2,000 in additional tax for those earning over $100,000 per year. • Third, the Alternative Minimum Tax has finally been indexed for inflation. This means Congress will no longer have to "patch" it every year to avoid entangling millions more taxpayers in its web. • Finally, the Medicare tax provisions of the Affordable Care Act, or "Obamacare," have taken effect. This means an extra 0.9% tax on earned income above $250,000 and a 3.8% tax on investment income for taxpayers earning more than $200,000 ($250,000 for joint filers). President Obama has called for slashing several more tax breaks, possibly including some sacred cows like mortgage interest. However, after the recent government shutdown, there appears to be little appetite on Capitol Hill for further changes to the code. With just 20 days left in until the “IRS Holiday Tax Sale” ends join us here to review some specific strategies for minimizing your tax under the new rules.  No IRS Black Friday deals today? No IRS Black Friday deals today? The day to give "Thanks" is behind us and the holidays are in full swing. Millions of Americans are kicking off the season with “Black Friday” shopping. Braving the crowds and the cold, facing scorn from family they’ve left behind, they line up at obscenely early hours (or duck out of Thanksgiving dinner before the pumpkin pie is even served) to save $20 on a iPad or $40 on a flat-screen television.

It’s sad, but true, that most Americans spend more time planning their “Black Friday” shopping than they spend planning their taxes. But that can be an expensive mistake! What if the IRS had a sale? What if the IRS let you discount your taxes by thousands of dollars, this year and every year to come? And what if they let you do it from the comfort of your home or your office, without lining up in the pre-dawn hours of a chilly November morning? Would you give thanks for a sale like that? You’re probably not holding your breath for the scrooges at the IRS to hold a “sale.” The good news is, you don’t have to wait for that to happen. You just need a plan. Tax planning is the key to paying the legal minimum. And a good tax plan can pay for a holiday season full of gifts and fun. Now is the season to find the mistakes and missed opportunities that may be costing you thousands. “Black Friday” tax planning before the year end can save thousands more off your taxes in the future. There are 31 days left for "Black Friday" tax planning. Contact us for ways to save on your taxes before the end of the year.  Many say that Friday the 13th is an unlucky day and today may be one of those days for taxpayers. It would appear that the IRS is playing the role of Jason Voorhees and are performing an all out massacre on the many tax deductions individuals and small business owners rely on to save money on their tax returns. Here are 13 (unlucky) tax deductions that the IRS will slaughter like Jason did the kids at Camp Crystal Lake by year end.

Don't want to be caught by the slashing machete of the IRS? Now is the time to put a plan in action so you will still be alive when the credits roll at the end of 2013. Time is ticking...

See how much time you have left here.  The Internal Revenue Service has modified its “first time abate” or (FTA) policy, which provides a one-time consideration of penalty relief, based on the taxpayer’s compliance history.

The FTA penalty relief option for failure to file, failure to pay and failure to deposit penalties, under certain conditions, does not apply if the taxpayer has not filed all returns and paid, or arranged to pay, all tax currently due. For example, the taxpayer is considered current if they have an open installment agreement and are current with their installment payments. The FTA relief only applies to a single tax period for a taxpayer, and penalty relief under the first time abatement provision does not apply to returns with an event-based filing requirement. Additionally the FTA relief does not apply to the following type returns if a previously filed return was late:

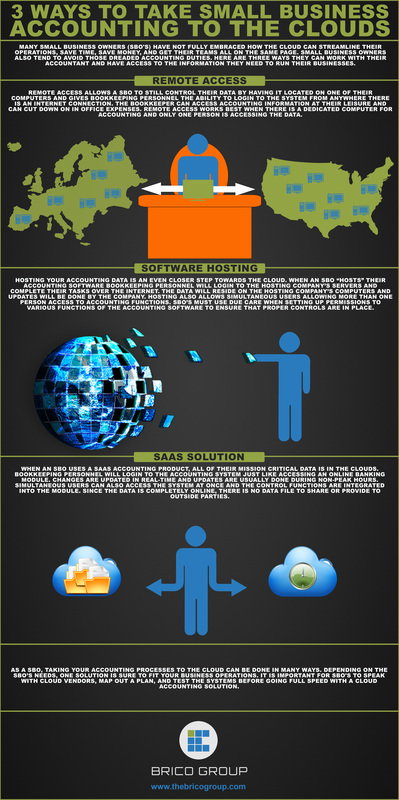

Feel free to contact us if you need assistance with a tax penalty abatement or proactive tax planning. Small business owners that are hearing a great deal about the cloud lately may not have all the facts when it comes to accounting in the cloud. Here is an infographic we created to outline the three major ways to take your accounting to the clouds.

In an attempt to reduce the administrative, recordkeeping, and compliance burdens of taxpayers, the IRS has offered a safe harbor method to compute the allowable deduction for the business-use portion of the home. The safe harbor method is effective for taxable years beginning on or after January 1, 2013.

Under the safe harbor method, the taxpayer multiplies the allowable square footage of the home office by the prescribed rate of $5.00. The allowable square footage for business use cannot exceed 300 square feet; thus, the maximum allowable home office deduction under the safe harbor method is $1,500. The safe harbor deduction, cannot exceed the business income for the year reduced by business expenses unrelated to the dwelling unit. Any taxpayer using the safe harbor method may not carry over any disallowed safe harbor deductions to the next year. Other Provisions

|

AuthorVarious contributors Archives

December 2023

Categories

All

|

RSS Feed

RSS Feed